Make-it Capital Edition #35

The World of Cryptocurrencies

Smart contract platforms such as Ethereum (ETH), Solana (SOL), and Avalanche (AVAX) have caught up with bitcoin (BTC) this month and produced a solid outperformance — a development the fund bet on even if we were one month early.

The hashrate reached another record high, solidifying the Bitcoin network even more which is always very welcome.

November also witnessed a revival of decentralized finance (DeFi) — up 15% as well as GameFi (Web3 gaming) reaching a market capitalization of nearly $15 billion. Both areas are very promising for the bullish phase we have now entered.

In the world of stablecoins, Tether (USDT) was able to expand its market dominance gaining another 6% in market capitalization reaching close to $90 billion.

The once promising BUSD, created by Paxos and supported by Binance, has fallen into oblivion following its condemnation by the SEC a few months ago. BUSD has lost around $22 billion in market capitalization and is likely to disappear altogether soon. After all, Binance will delist and will end support for BUSD in a few weeks. Filling the void are DAI and newcomer from Hong Kong FDUSD, gaining 43% and 106% in market capitalization respectively in November.

Fidelity, one of the world’s largest asset managers with $4.3 trillion in assets under management and $10.3 trillion in assets under administration (as of December 2022), has debunked a number of unfounded Bitcoin criticisms in its latest report “Persistent Bitcoin Criticisms”. It’s definitely worth taking the time to read, and a secure link to the original report has been included below. Here is a brief sample:

Criticism #1: Bitcoin is too volatile to be a store of value.

Response: Bitcoin’s volatility is a trade-off for perfect supply inelasticity and an intervention-free market. Bitcoin’s volatility is a trade-off for a distortion-free market. True price discovery accompanied by volatility might be preferable to artificial stability that may then lead to distorted markets that may break down without intervention. Quite true.

Moving to Sam Bankman-Fried or SBF of FTX who was finally fried. Whether he will see the light of day again in his lifetime remains to be seen, but it’s important to note that this whole episode has nothing to do with cryptocurrencies as an asset class. Crypto is not to blame for FTX’s disaster. That would be like blaming equities for the Enron scandal. US Attorney Damian Williams put it well when he said, “These players like Sam Bankman-Fried might be new, but this kind of fraud, this kind of corruption, is as old as time.”

Regardless of birthing pains, crypto and blockchain technology are going to disrupt our world as the internet and mobile phone industries have before. Probably even more so. Here is an interesting overview of adoption times across various disruptive technologies:

- The radio was invented in the 1890s and introduced in the 1920s.

- Television was invented in 1902, but only came into households in the 1950s.

- Email was invented in 1969 and it took until 1997 for it to be used.

TCP/IP — the base layer Internet protocol — was developed in 1970 as a DARPA (Defence Advanced Research Projects Agency) project. In 1983, TCP/IP was accepted as the standard internet protocol. Thus, it took 13 years to get there — exactly where Bitcoin is now.

It then got commercially accepted another 12 years later in 1995 with the introduction of Windows 95. With a market capitalization of $750 billion one could assume that Bitcoin has already reached commercial adoption.

The foundation for the future of blockchain technology has been laid with several layer 1 and layer 2 blockchains. Now the applications will follow suit. Which will be the Windows 95 for blockchain?

As Andrew Durgee president of Republic said in front of Congress: “Adoption at this stage is not a technology problem it is a human conditioning issue.”

The day of the final decision on the spot Bitcoin ETF applications in January is fast approaching. The big question is how much interest there will be in Bitcoin ETFs when they are launched.

Crypto data firm Glassnode predicts that Bitcoin, as a digital store of value, could attract some of the gold investors. The company estimates that a total capital flow of $70.5 billion could flow into Bitcoin, including about $9.9 billion from the gold market.

In any case, such new capital inflows will have a significant impact on the Bitcoin price (and upon its respective approval also on the ETH price) in fiat currencies.

The World of Commodities

Silver outperformed gold as we had ventured to predict it would last month, reducing the gold/silver ratio from 87 to a more normal 80. By rising 5% Dr. Copper suggests the economy is picking up steam while natural gas lost an astounding -20% in November and -56% year over year, respectively, which has been attributed to record production, high inventories, and a mild winter.

Oil prices continue to trend downwards as OPEC+ cuts fail to convince oil traders due to lack of detail. The alliance decided on the cuts at a recent online meeting, but their final communiqué did not address the cuts. In separate statements, Saudi Arabia pledged to continue its unilateral cut of 1 million barrels per day through the first quarter, while other countries such as Russia and Kuwait released details of their individual cuts.

The lack of a comprehensive breakdown combined with the “voluntary” nature of the cuts did not convince market observers.

“Crude is cratering because so far traders have yet to see concrete evidence of credible incremental output cuts alongside the continuation of voluntary Saudi and Russian cuts,” said Bob McNally, president of Rapidan Energy Group. The market is “surprised and confused, pending clarity.”

In the meantime, the US has reached a record production of 13.236 million barrels per day, according to the latest statistics published by the EIA.

As for other commodity-related developments, we must again draw attention to lithium, which has lost another -27%, bringing its year-on-year loss to almost -80%. The EV revolution seems to be stuttering somewhat.

The largest price increases were recorded for potatoes, which rose by 46% this month, and eggs, which almost doubled in November. It might be better to start the day with some classical porridge …

The Rest …

Western equity markets returned to full bull mode in November flirting with or even beating double-digit price rises.

At present, the market is convinced of the return of Goldilocks wealth, which means that the slowdown in economic activity will be mild, and inflation will continue to fall towards trend without any negative surprise. The big question is whether the slowdown in employment growth will intensify. In addition, the slowdown in the transportation of goods, as evidenced by the reversal in the Dry Baltic Index, is usually a sign that consumption is about to decline. We all love the Goldilocks constellation, but we remain somewhat skeptical.

Then again, Marty Zweig was perhaps most well known for warning Wall Street Week viewers that he didn’t like what he saw in the market just before Black Monday in 1987.

The indicator he created, the Zweig Breadth Thrust (ZBT), is calculated by the 10-day moving average of the percentage of rising stocks on the New York Stock Exchange. A move from 40% to 60% in 10 days or fewer triggers the “buy” signal.

According to the ZBT, a perfect bullish sign just triggered for only the 18th time since World War II…

And according to data from Carson Investment Research, stocks were higher six months later in every case. Well …

Moving on to the meanwhile scary levels of private credit card debt.

As we know, consumer spending is the most important engine of growth, accounting for about two-thirds of total economic activity in Western hemispheres. It seems that the ubiquitous pandemic checks have been spent and consumption is entirely debt based. After all, credit card debt recently surpassed the $1 trillion mark in the US alone. At current interest rates, this means that the average consumer is paying 21% interest on this debt in addition to the principal. Total credit card debt has thus increased by nearly $300 billion in the last two and a half years. That sounds scary.

However, there is another side to the coin: assets in the form of private sector checkable deposits, i.e. cash.

According to the latest figures from the St. Louis Fed, this figure now stands at almost $5 trillion, up from $1.5 trillion in the fourth quarter of 2019. Thus, the ratio of private credit card debt to cash is at around 20%, the lowest level since 2000. This puts the dramatic-sounding $1 trillion in credit card debt into perspective. It seems that the engine of the economy has enough fuel to keep running for quite some time.

Lending money without being a bank is becoming a big business. Known in investor jargon as private debt, this market niche has increased sharply in recent years. Private credit funds, which collect money from large investors and then lend it on, have multiplied in volume in recent years: before the GFC (global financial crisis) in 2008, the market volume stood at $235 billion, today it is estimated at $1.6 trillion. The rapid growth and size of the market is now also alarming the German financial supervisory authority Bafin.

The supervisory authority fears that “private credit funds could pose risks for consumer protection, market integrity and financial stability”. Bafin is not alone in its skepticism. Colm Kelleher, Chairman of the Board of Directors of the major Swiss bank UBS, recently said about private debt: “I believe the next crisis, when it breaks out, will be in this sector”.

If you then add the whole area of shadow banking to the picture, it gets really scary. Shadow banking is the term for financial intermediaries outside the banking sector such as money market funds, hedge funds and private loans. These players are also known as non-bank financial companies (NBFCs) and operate with little or no oversight from financial regulators. This is a wild west market with unknown trillions of fiat currency at stake. Pretty petrifying and another reason to hold a 1–5% allocation to decentralized money, aka cryptocurrencies.

MAKE-IT CAPITAL FUND (the Fund)

- As a unique hedge fund for a comprehensive blockchain / cryptocurrency portfolio, the Fund allows investors to participate in the full spectrum of distributed ledger/crypto assets with just one investment.

- The Fund set out to reduce inherent risk and volatility by employing its proprietary 5-pillar strategy.

- The Fund is operated by Make-It Singapore and managed by Make-It New Zealand.

- It is open to institutional and accredited investors worldwide.

- Open-end structure with a minimum investment of $50,000.

- The Fund is fully transparent and always trades at the exact NAV.

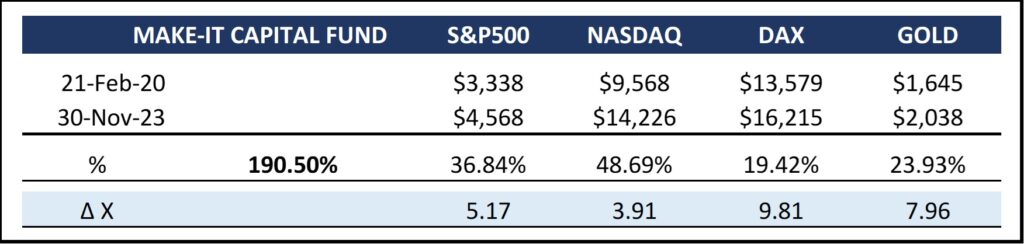

The Fund continues to develop positively and is once again outperforming Bitcoin. We are currently developing a new and more sophisticated arbitrage system as one of our five pillars. We are very much looking forward to launching this product as part of the Fund in January 2024 and will report on progress on these pages.

Switching ears. While Meta and X/Twitter laid off employees a year ago, Wall Street hired new ones. JPMorgan Chase, for example, invested $12 billion into this push and housed more than 50,000 engineers, developers and technologists.

The vast majority of these tech-savvy employees are working on just one thing: tokenization, programmable money, interoperability… Which are just fancy euphemisms for blockchain technology.

Blockchain technology is not just about cryptocurrencies. That would be like saying the internet is just about email. Rather, it is a profoundly revolutionary financial technology that will turn the financial world order on its head.

That is why we have placed the Fund on its five pillars: to cover the entire world of blockchain technology, not just cryptocurrencies in order to capture as much upside of the entire ecosystem as possible.

Thank you for your time and attention.

Sincerely,

Philipp L.P. von Gottberg

P.S. Here is the promised safe link to the recent Fidelity report:

Revisiting Persistent Bitcoin

Criticismshttps://www.fidelitydigitalassets.com/sites/default/files/do…